[ad_1]

Sky_Blue/iStock Unreleased via Getty Images

It’s rare to find companies that have cult-like followings with loyalists willing to pay any price for its stock. The debate regarding Tesla, Inc.’s (NASDAQ:TSLA) valuation continues to be a topic of conversation between the bulls and the bears. One side argues that TSLA’s financial growth and future prospects, including FSD, insurance, and robotaxis, justify the current $902.12 billion valuations, while others argue that the current financials and cult-like following have led to a massive overvaluation in TSLA’s stock.

I tip my hat to Elon Musk, as his accomplishments are second to none. When others called him crazy, Mr. Musk chose one of the hardest industries to compete in, started TSLA from the ground up, went to battle against the auto manufacturers, and succeeded. TSLA is one of the rare success stories that has truly shaped an industry, and the barriers of entry that were overcome are astonishing. TSLA didn’t have the capital, manufacturing, credibility, or the infrastructure that its competitors did, yet they found a way to succeed. If the odds weren’t enough which TSLA faced, they accomplished their goals without a combustible engine and pioneered an entirely new sector within the automotive industry.

Just because TSLA is a great company, it doesn’t mean TSLA has a great stock, or it isn’t overvalued. I am not bearish on TSLA the company because I believe they still have a long runway of growth ahead of them, but I am bearish on the valuation. Prior to leaving a comment on why I am wrong, please read the article and think about the metrics I am citing; then, I will happily discuss any viewpoints about the analysis.

Tesla

Tesla Vs. The World In The Automotive Sector

It feels like TSLA vs. the world whenever TSLA is discussed. Discussing who makes a better automobile is a matter of opinion, and everyone is correct because it’s their opinion. If person A thinks TSLA makes the best car and person B thinks Mercedes Benz makes the best car, they are both correct. Debating over this is pointless, so let’s look at the raw numbers.

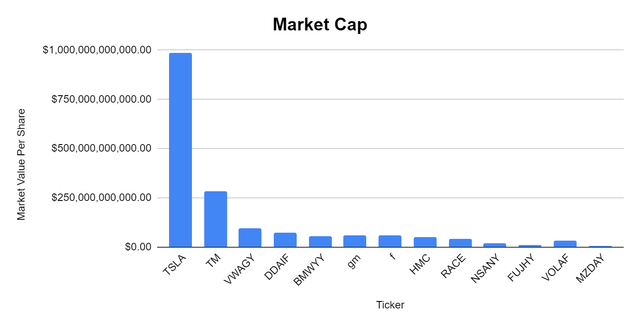

TSLA has a larger market cap than the combination of Toyota (TM), Volkswagen (OTCPK:VWAGY), Daimler (OTCPK:DDAIF), BMW (OTCPK:BMWYY), General Motors (GM), Ford (F), Honda (HMC), Ferrari (RACE), Nissan (OTCPK:NSANY), Subaru (OTCPK:FUJHY), Volvo (OTCPK:VOLAF), and Mazda (OTCPK:MZDAY). TSLA’s market cap is currently $986.92 billion, while the combination of these 12 companies is $777.41 billion.

Steven Fiorillo

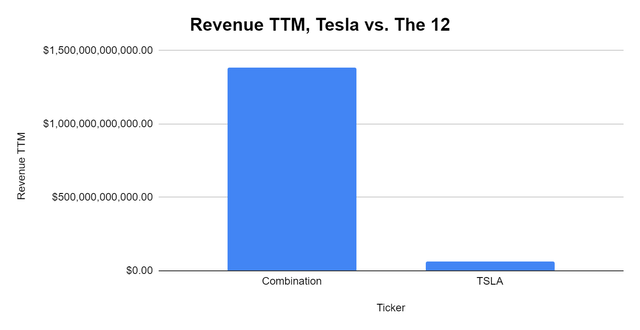

The P/S ratio is often cited to justify the valuation. The combination of TM, VWAGY, DDAIF, BMWYY, GM, F, HMC, RACE, NSANY, FUJHY, VOLAF, and MZDAY has generated $1.38 trillion in revenue over the TTM, putting their P/S at 0.56, while TSLA has generated $62.19 billion in revenue and has a 15.87 P/S.

Steven Fiorillo, Seeking Alpha

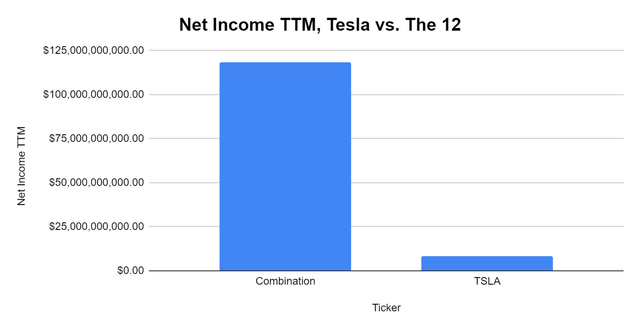

As a combined entity, these 12 companies have generated $118.29 billion in net income, while TSLA has produced $8.4 billion.

Steven Fiorillo, Seeking Alpha

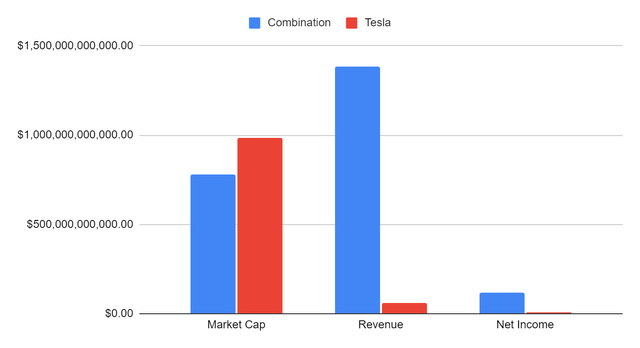

TSLA is a great company, but its current valuation has become overly inflated. TSLA’s market cap is $209.52 billion larger than these 12 auto manufacturers, yet the combination of the 12 auto manufacturers generates $1.32 trillion more in revenue and $109.89 billion more in net income.

Steven Fiorillo, Seeking Alpha

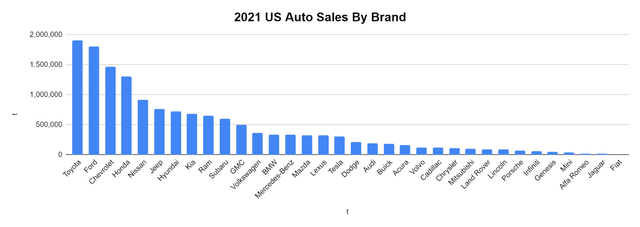

Looking at the market caps, one would assume that TSLA has a dominant majority over its competitors in auto sales within the U.S. According to the 2021 data, TSLA sold 2.02% of all vehicles in the U.S. TSLA’s market cap reflects a level of dominance that is non-existent.

Realistically, TSLA will have a hard time disrupting the sector further due to the price point of their vehicles. The reality is that, unless TSLA can sell a car that rivals a Honda or Toyota, doubling its market share is going to be a daunting task. It’s just math. TSLA doesn’t have a product for the masses, and while it may continue to grow in the luxury segment, the amount of growth that can be achieved is limited due to the pricing power of the consumer.

www.goodcarbadcar.net

Tesla Isn’t A Technology Company And Shouldn’t Be Valued As One

The valuation rebuttal has always been that TSLA isn’t an automobile company, rather, it’s a technology company.

Tesla

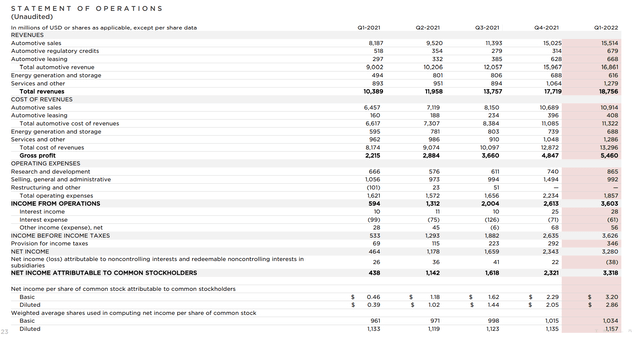

Page 23 of TSLA’s Q1 2022 slide deck from their earnings call is their statement of operations. Once again, 100% of TSLA’s gross profit and net income are derived from automobiles. Energy generation and storage lose money as it generates $616 million in revenue while the cost of this revenue is $688 million. The same goes for Services and others, as this segment generates $1.279 billion in revenue while the cost of this revenue is $1.286 billion. This doesn’t even factor in operating expenses.

TSLA manufacturers state of the art automobiles, but this doesn’t classify them as a technology company, nor should they be classified as one. Since this is always the rebuttal and technology companies trade at larger earnings multiples, I will compare TSLA to Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Meta Platforms (FB) and illustrate why TSLA is still drastically overvalued if the market was still to provide it with a tech multiple.

Prior to the comparisons, I want to frame the analysis by providing each company’s market cap:

- AAPL $2.69 Trillion

- MSFT $2.17 Trillion

- GOOGL $1.62 Trillion

- AMZN $1.28 Trillion

- TSLA $986.92 Billion

- FB $604.62 Billion

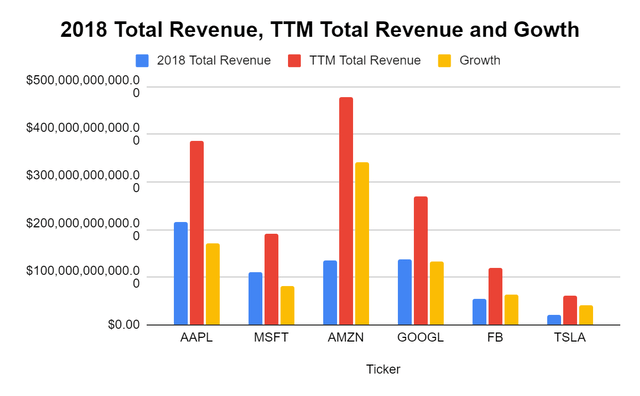

I am going to start with growth because this is always the key metric bulls point out. Since the close of 2018, which is 3.25 fiscal years, TSLA has grown its revenue from $21.46 billion to $62.19 billion.

This is absolutely remarkable, but it doesn’t place TSLA in the upper epsilon of technology companies. Over the same period, FB grew its revenue by $63.83 billion, which is more than what TSLA produced in the TTM. FB grew its revenue by more than what TSLA produces and generates just about double the revenue ($119.67 billion), yet TSLA has a larger market cap. For everyone who has used growth as their investment premise, FB having a market cap that’s $382.30 less than TSLA nullifies that aspect of the bull thesis. AMZN’s market cap is only $294.33 billion larger than TSLA, yet they generated $477.75 billion in revenue and grew their revenue by $341.76 billion in this period. Using revenue growth for TSLA doesn’t support the valuation.

Steven Fiorillo, Seeking Alpha

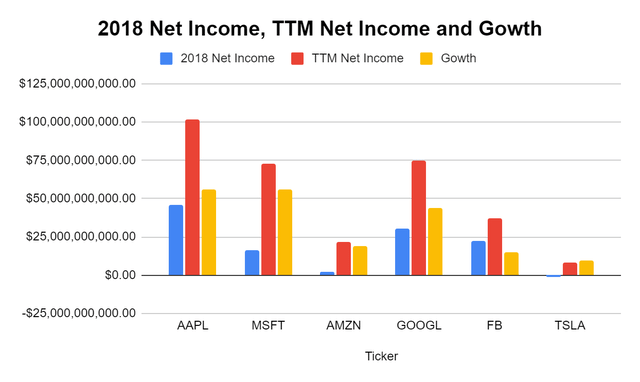

Next, I will turn to profits because, at the end of the day, businesses are in the business of making money. Once again, TSLA has done a fantastic job of monetizing its business and, in 3.25 short years, has gone from losing -$976 million to make $8.4 billion in the TTM for an increase of $9.38 billion. FB has produced $37.34 billion in profit in the TTM, and its net income grew by $15.23 billion over this period. Using growth doesn’t support the valuation when FB has a market cap that’s $382.30 less than TSLA and grew its profits in this period by almost double what TSLA has generated in the TTM.

Steven Fiorillo, Seeking Alpha

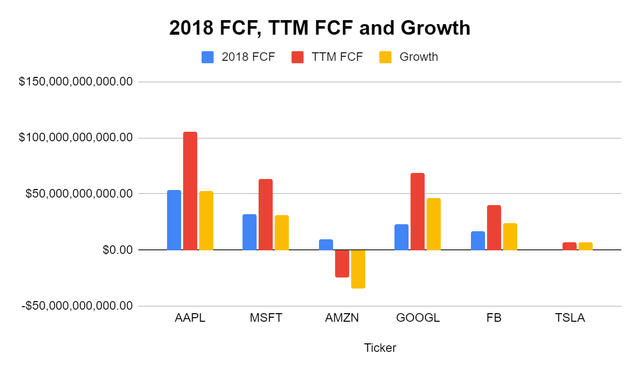

The new metric bulls are using in their thesis is TSLA’s free cash flow (FCF). Once again, TSLA has done an excellent job, going from -$221 million of FCF in 2018 to $6.93 billion of FCF in the TTM. Many companies would love to grow their annual FCF by $7.15 billion over a 3.25-year period, and this should be applauded.

Let’s look at FB once again, since TSLA’s valuation isn’t based on its core segment as an automobile manufacturer. FB has grown its FCF over the previous 3.25 years by $23.45 billion, more than 3x TSLA’s growth, and has generated $39.81 billion of FCF in the TTM. FB generated roughly 5.75x more FCF than TSLA and grew its FCF by more than 3x what TSLA produces, yet FB has a market cap that’s almost $400 billion less than TSLA. Growth within the financials does not support TSLA’s valuation, which is a breath away from $1 trillion.

Steven Fiorillo, Seeking Alpha

Today you’re paying a 113.81 P/E for TSLA. Paying a larger multiple for a company that’s growing its earnings quickly is normal, but TSLA isn’t growing by larger amounts than FB, and FB trades at a 16.66 P/E. I have seen TSLA bulls justify the P/E because of TSLA’s growth factor, but this doesn’t hold up when FB has grown by larger amounts from larger starting positions and has a P/E that’s a fraction of TSLA. Look at AAPL, which is the largest company in the world. AAPL has grown its net income by $56.25 billion and its FCF by $52.3 billion over the past 3.25 years, and its P/E is 26.78. People are blindly paying any multiple the market places on TSLA.

|

Price to Earnings |

|||

|

Ticker |

Market Value Per Share |

Earnings Per Share |

P/E Ratio |

|

AAPL |

$166.02 |

$6.20 |

26.78 |

|

MSFT |

$289.98 |

$9.58 |

30.27 |

|

AMZN |

$2,518.57 |

$41.36 |

60.89 |

|

GOOGL |

$2,445.22 |

$112.19 |

21.80 |

|

FB |

$223.41 |

$13.41 |

16.66 |

|

TSLA |

$952.62 |

8.37 |

113.81 |

TSLA is trading at a 15.38 P/S. The justification for this multiple is difficult to defend while AMZN trades at a P/S of 11.31. AMZN’s revenue grew by $341.76 billion over the past 3.25 years while TSLA grew their revenue by $40.73 billion. Instead of an absolute basis, looking at this from a percentage aspect, TSLA grew its revenue by 189.78%, while AMZN’s grew by 251.32%. The P/S ratio is not a supporting valuation metric as TSLA is trading at a larger multiple than AMZN yet produced $301.03 billion less in revenue growth compared to AMZN. At the very least, TSLA should trade at a lower P/S multiple than AMZN considering their revenue growth was a fraction of AMZN’s.

|

Price to Sales |

|||

|

Ticker |

Market Value Per Share |

Revenue Per Share |

P/S Ratio |

|

AAPL |

$166.02 |

$23.47 |

7.07 |

|

MSFT |

$289.98 |

$25.64 |

11.31 |

|

AMZN |

$2,518.57 |

$941.84 |

2.67 |

|

GOOGL |

$2,445.22 |

$406.89 |

6.01 |

|

FB |

$223.41 |

$42.98 |

5.20 |

|

TSLA |

$952.62 |

$61.93 |

15.38 |

TSLA has done an excellent job monetizing its revenue, delivering exceptional margins, and generating FCF. Now that TSLA is generating billions in FCF, it’s been inserted into the bull thesis. FCF is a measure of profitability that excludes the non-cash expenses of the income statement and includes spending on equipment and assets as well as changes in working capital from the balance sheet. FCF could be the most underrated and most important financial metric to look at, as this is the pool of capital that companies can utilize to repay debt, pay dividends, buy back shares, make acquisitions, or reinvest in the business.

Every investment is the present value of all future cash flow. This is why investors look at the price to FCF valuation. Investors want to pay the cheapest multiple for a company’s FCF. Today, you’re paying 142.52x TSLA’s FCF. Going back to the FCF section, TSLA grew its FCF by $7.15 billion over the past 3.25 years. FB generated $23.45 billion of FCF in this period, which is 3x the amount TSLA grew, yet FB is trading at a 15.19x multiple on price to FCF.

Why on earth would you want to pay 142.52x for TSLA’s FCF when you could pay 15.19x for FB, which is growing their FCF by more than 3x the amount that TSLA is growing by? How about AAPL? AAPL grew its FCF by $52.3 billion and trades at a 25.4x price to FCF. If I exclude FB for a moment, should TSLA trade at a larger FCF multiple than GOOGL, which has grown its FCF by $46.15 billion over the past 3.25 years? My answer is no because there is no guarantee that TSLA will ever generate $46.15 billion in annual FCF, let alone the $68.99 billion in FCF that GOOGL generates.

So what is a fair price to FCF multiple for TSLA? I don’t believe TSLA has earned the right to trade at the same multiples as the rest of big tech considering the levels of FCF they produce. If I stick with the methodology that FB is egregiously undervalued, then TSLA should trade above 15.19x its FCF but lower than the 23.42x multiple GOOGL trades at.

I don’t want to be overly bearish, so I will place a 21x multiple on TSLA’s FCF, which is more than fair considering big tech metrics. A 21x multiple on TSLA’s FCF puts its market cap at $145.43 billion, which is -85.26% from its current market cap of $986.92 billion. It’s just math, and if TSLA is going to be valued as a technology company, it needs to be compared to the technology companies with similar market caps.

At the very least, there isn’t a single reason why TSLA’s market cap is larger than FB’s. There isn’t a single metric that TSLA beats FB in. Based on FB’s valuation, if TSLA traded at the same FCF multiple, it would have a market cap of $105.19 billion.

|

Price to Free Cash Flow |

|||

|

Ticker |

Market Cap |

Total Free Cash Flow |

Price to Free Cash Flow Multiple |

|

AAPL |

$2,687,063,652,750.00 |

$105,793,000,000.00 |

25.40 |

|

MSFT |

$2,168,770,071,507.00 |

$63,649,000,000.00 |

34.07 |

|

AMZN |

$1,281,247,972,603.00 |

-$24,598,000,000.00 |

|

|

GOOGL |

$1,615,371,731,491.00 |

$68,985,000,000.00 |

23.42 |

|

FB |

$604,619,631,340.00 |

$39,812,000,000.00 |

15.19 |

|

TSLA |

$986,922,888,521.00 |

$6,925,000,000.00 |

142.52 |

TSLA has a gross profit margin of 27.1% ($16.85b / $62.19b) and a profit margin of 13.51% ($8.4b / $62.19b). FB has a gross profit margin of 80.34% ($96.14b / $119.67b) and a profit margin of 31.2% ($37.34b / $119.67b). FB has much wider margins and is growing its revenue by larger amounts. This reinforces my methodology as to why TSLA is grossly overvalued. GOOGL has a gross profit margin of 56.93% ($153.9b / $270.33b) and a profit margin of 27.57% ($74.54b / $270.33b).

The chances are incredibly slim that TSLA can double its profit margin to be within striking distance of GOOGL’s. TSLA should not trade at a larger FCF, P/E, or P/S multiple than FB or GOOGL. While the market would indicate that I am wrong today, eventually, the hype will wear off, and TSLA will trade at a realistic valuation.

TSLA’s Future Catalysts Have A Long Way To Go Before Impacting Its Bottom Line

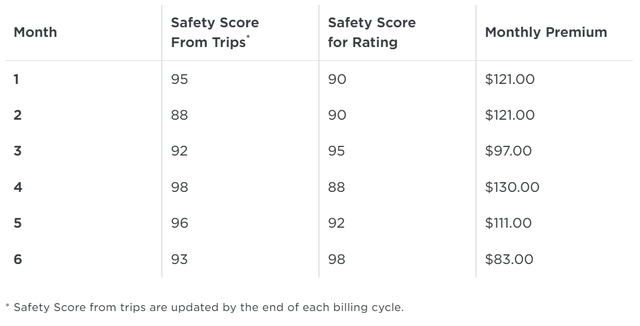

There are three main catalysts people discuss, which include insurance, robotaxis, and FSD. TSLA offers insurance using real-time driving behavior. This is currently available to all Model S, Model 3, Model X, and Model Y owners. The catch is that it’s only available in Arizona, Colorado, Illinois, Ohio, Oregon, Texas, and Virginia as of now.

TSLA uses a safety rating score to determine the monthly premium for its vehicles. At the largest premium of $130/mo, this would be $1,560 per year. If TSLA converted 100% of their U.S sales in 2021 as an insurance customer, which I think could be possible if TSLA insurance was available in every state, it would have generated $471.12 million in revenue.

We have no idea what the margins would have been, but if the margin was 50%, it would have been an additional $235.56 million in net income in 2021. While this is nothing to sneeze at, an additional $235.56 million in net income hardly moves the needle. This could be a $1 billion top-line revenue segment in the future, but with availability in only 7 states, insurance’s $1 billion revenue mark is a long way away.

Tesla

Next, FSD, for which TSLA has created two subscription models, a $99/mo price point and a $199/mo price point. The problem with FSD is that it doesn’t make the vehicle fully autonomous, and you still need a driver to be attentive and alert. While I am not arguing that TSLA’s FSD isn’t leaps and bounds ahead of the competition, the problem is that it’s not exactly a self-driving car.

The questions around legality and where you can use it pop into my head, and how many of TSLA’s drivers opt for this upgrade. Until there is clear legislation and the technology advances to where vehicles can fully drive a person from point A to B while that person takes a nap or reads, I have a hard time believing enough TSLA owners will spend the extra $199/mo on FSD. If there is somewhere where TSLA produces the numbers about how many owners opt for this package, please let me know, and I will crunch the numbers.

Which Features Come With My Subscription?

The FSD capability features you receive are based on your configuration and location. Not all features are available in all markets, and features are subject to change. Learn more about Autopilot and Full Self-Driving capability features.

Note: These features are designed to become more capable over time; however the currently enabled features do not make the vehicle autonomous. The currently enabled features require a fully attentive driver, who has their hands on the wheel and is prepared to take over at any moment.

The last catalyst is Robotaxis which many have commented on in my articles before. We’re so far off on Robotaxis that this can’t be considered in TSLA’s upcoming revenue. I would think major legislation would be needed for Robotaxis to exist, and there is no telling how many years away we are from this.

Also, what is the percentage of TSLA owners that would actually allow their vehicle to be used as a Robotaxi? Depending on what the profitability is, I can see people buying TSLAs to enroll them in this program, but, once again, we need to see the economics behind it. I know I am just one opinion, but I would never enroll one of my cars into a robotaxi program because I don’t want other people that I don’t know in my car. I would think there are many others that have similar viewpoints.

The real upcoming catalysts are future revenue growth and entering the Chinese market. In 2021 TSLA grew its YoY revenue by 70.67%, and their off to a great start after Q1 2022. Only time will tell what type of growth rate TSLA can maintain, but too many people are assuming that TSLA will obliterate the competition. Over the next several years, we could see TSLA’s growth rate become significantly reduced as more luxury operators put EVs on the road.

At TSLA’s current margins, they would need to increase their revenue by 444.55% to $276.47 billion to produce the same amount of net income ($37.34b) that FB produces today at their current 13.51% profit margin. Maybe TSLA can get there in the future, but why should TSLA be valued at almost $1 trillion today, considering not a single metric of theirs is similar to FB or GOOGL, and TSLA’s growth across any of the sectors isn’t larger than FB or GOOGL?

Tesla

Tesla Continues To Dilute Shareholders, And Almost No Shareholders Care

Dilution kills shareholder value. Look, I am a shareholder of TSLA, and I hate that my shares continue to be diluted. These numbers are split-adjusted that I am using. Over the past decade, TSLA has diluted its shares by 80.93%. This is horrible compared to big tech, yet investors can’t buy enough TSLA shares. TSLA finished 2012 with 572.6 million shares and, as of its last filing, had increased its outstanding shares to 1.036 billion shares.

This is the equivalent of me taking a pizza, and instead of giving you a slice, cutting another 6.5 slices, then giving you one. The pizza represents TSLA, the company, and they basically turned an 8-slice pie into a 14.5-slice pie, reducing shareholder’s ownership and the amount of equity, revenue, and EPS our shares represent.

If you want to see what a true shepherd of shareholder value looks like, turn to AAPL. In 2012 AAPL had 26.3 billion shares outstanding. Over the past decade, AAPL has repurchased 10.09 billion shares, reducing its outstanding shares by 38.37%. Every quarter, AAPL is buying back shares and increasing the ownership its shares represent. TSLA, on the other hand, continues to dilute shareholders by increasing shares YOY.

I Could Be Completely Wrong, And Tesla Could Continue Growing At These Rates

TSLA’s vehicle deliveries continue to outpace its growing production. YoY TSLA’s deliveries increased by 68% in Q1, adding 125,171 delivered vehicles to its customers. TSLA just began Model Y deliveries from the Austin facility, and production at the Gigafactory in Berlin started in March of 2022. TSLA’s Shanghai facility had strong production rates prior to the spike in COVID that resulted in temporary shutdowns. TSLA isn’t just focusing on the U.S, they have Europe and China in their sights.

EVs accounted for 488,000 sales in the U.S for 2021, and the previous projection was that EVs would account for 670,000 units sold in 2022. Oil has hovered around $100 per barrel and could render the previous projections of 37% increased EV sales domestically for 2022 conservative. TSLA is in a prime position to capitalize on this trend. In 2021 TSLA vehicles accounted for 61.89% of EVs sold in the U.S (301,998 / 488,000).

Hypothetically, if the previous projection of 670,000 EV sales for 2022 is accurate and TSLA maintains its current margin, they would sell 414,628 vehicles throughout the U.S in 2022. If gas prices do alter the decision-making process when deciding between a combustible engine or an EV, then TSLA could continue surprising the market with QoQ earnings beats.

The U.S has a national goal of reaching 50% of domestic auto sales coming from EVs. In 2021, EVs accounted for 3.26% of total sales in the U.S auto market. Based on U.S auto sales in 2021, annual EV sales would need to grow by 6,989,403 to reach a 50% EV to combustible engine ratio. Hypothetically if U.S auto sales stayed flat but EVs reached 50% of the market in 2030 they would sell 7,477,403 vehicles. If TSLA’s dominance in the EV sector was to drop from 61.89% to 15% due to increased competition, they would generate 1,121,610 in sales compared to 301,998 in 2021. When you add in Europe and China, TSLA certainly has the ability to become a top auto manufacturer by sales next decade.

Bulls aren’t incorrect to be excited about TSLA. The world is moving toward EVs, and TSLA is the crème de la crème. As I said in the beginning, I am bullish about TSLA’s future prospects, but I think the valuation today is overinflated. Nobody can predict the future, but I have no doubt that TSLA will continue to grow its sales YoY.

The question becomes, how much growth will they be able to achieve YoY? In 2021, TM generated $226.48 billion of revenue and, based on the future of EVs, TSLA certainly could achieve this level of revenue in the future. Based on TSLA’s current 13.51% profit margin, if they achieved TM’s level of revenue, they would generate $30.59 billion of net income, which would definitely make today’s valuation look more realistic.

Tesla

Conclusion

You’re probably wondering how I can be a shareholder and be a bear on TSLA’s valuation at the same time. It’s simple; my wife bought shares of TSLA, which makes me a shareholder. My stance has always been bullish on the company and bearish on the valuation. What Elon Musk and the team at TSLA has accomplished is astonishing, and they deserve nothing but respect.

Keep in mind a company and a company’s stock are two separate things. TSLA continues to dilute shareholders, and they and the market are valuing TSLA as if it’s FB or GOOGL. TSLA is not a technology company; it’s an automobile company, as the automotive segments drive 100% of its gross revenue and net income.

TSLA is trading at a P/E of 113.81, a P/S of 15.38, and a 142.52x multiple on its FCF. The numbers are drastically inflated as TSLA has no business trading at a larger P/S multiple than AMZN, which trades at 11.31 P/S when it has grown its revenue by $341.76 billion over the previous 3.25 years compared to TSLA’s $40.73 billion of revenue growth. TSLA has generated $6.93 billion in FCF over the TTM, while Mr. Market has placed a 142.52x multiple on TSLA due to $7.15 billion FCF growth over the past 3.25 years. FB trades at a 15.19x FCF multiple while growing FCF by $23.45 billion over this period which is more than 3x what TSLA has generated in the TTM.

With FB trading at 15.19x FCF, GOOGL at 23.42x FCF, and AAPL at 25.4x FCF, it’s hard to justify any number above 20x for TSLA. I think a 21x FCF multiple is generous and that places TSLA at a market cap of $145.43 billion, which is -85.26% from its current market cap of $986.92 billion.

[ad_2]

Source link